Simplify your loan repayment journey with our essential tools, including the Simple Interest Loan Payment Calculator or Simple Interest Only Loan Calculator. This powerful calculator will help you evaluate your loan options, plan your budget, and make informed decisions, empowering you to navigate your financial obligations with ease and achieve a secure financial future.

Simple Interest Loan Calculator

What is Simple Interest?

Simple interest is a basic calculation of interest, based on the principal amount borrowed or invested. It is a fixed percentage of the principal amount, and is generally expressed as an annual percentage rate (APR). For example, if the APR is 5% and the principal amount is $1,000, the simple interest for one year would be $50.

Simple Interest Formula – How is Simple Interest Calculated?

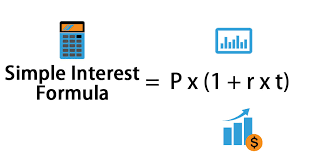

The formula for calculating simple interest is:

Simple Interest = P x r x t

Where:

- P is the principal amount

- r is the interest rate as a decimal

- t is the time period in years

The formula is quite simple and involves multiplying the principal amount by the interest rate and the time period.

Example 1: Let’s say you borrow $5,000 at a simple interest rate of 4% for 3 years. Using the formula, the calculation would be:

Simple Interest = $5,000 x 0.04 x 3 = $600

In this example, the simple interest on the loan would be $600 over the three-year period.

Example 2: Now, let’s consider an example of investing. If you invest $10,000 in a simple interest savings account that earns an annual interest rate of 2%, the calculation would be:

Simple Interest = $10,000 x 0.02 x 1 = $200

In this example, the simple interest earned on the investment for one year would be $200.

Why is the Simple Interest Formula Important?

The simple interest formula is important because it allows borrowers and investors to calculate the amount of interest they will earn or pay on a loan or investment. It is an essential tool for making informed financial decisions.

In addition, the simple interest formula is also useful because it is easy to use and understand. It is a basic calculation that can be done by hand or using a simple calculator.

In conclusion, the simple interest formula is a basic but essential tool for borrowers and investors. It allows individuals to calculate the amount of interest they will earn or pay on a loan or investment, and is easy to use and understand.

What Financial Instruments Use Simple Interest?

One common type of interest used in financial instruments is simple interest. In this article, we will discuss what financial instruments use simple interest.

Before we dive into the financial instruments that use simple interest, let’s review what simple interest is. Simple interest is a type of interest that is calculated only on the principal amount, without taking into account any interest that has already been earned. It is calculated based on the principal amount, interest rate, and time period.

Now that we know what simple interest is, let’s take a look at some financial instruments that use this type of interest:

Personal Loans

Personal loans are a common type of financial instrument that use simple interest. When you take out a personal loan, the lender will charge you interest based on the principal amount, interest rate, and time period. The interest rate on personal loans can vary depending on your credit score, the amount of the loan, and other factors.

Auto Loans

Auto loans are another financial instrument that commonly use simple interest. When you purchase a car using an auto loan, the lender will charge you interest based on the principal amount, interest rate, and time period. The interest rate on auto loans can also vary depending on factors such as your credit score, the age of the car, and the loan term.

Mortgages

Mortgages are a type of financial instrument that use simple interest as well. When you purchase a home using a mortgage, the lender will charge you interest based on the principal amount, interest rate, and time period. The interest rate on mortgages can vary depending on factors such as the type of mortgage, your credit score, and the length of the loan.

Savings Accounts

While loans may be the most common financial instruments that use simple interest, savings accounts also use this type of interest. When you deposit money into a savings account, the bank will pay you interest based on the principal amount, interest rate, and time period. The interest rate on savings accounts can vary depending on the bank and the type of account.

There are a variety of financial instruments that use simple interest. Personal loans, auto loans, mortgages, and savings accounts are just a few examples.

Simple Interest Versus Compound Interest

When it comes to interest rates, there are two main types: simple interest and compound interest. While they may sound similar, there are some key differences between the two. In this article, we will discuss the differences between simple interest and compound interest, and when each type is used.

Simple Interest

Simple interest is a type of interest that is calculated based on the principal amount, interest rate, and time period. The interest is calculated only on the principal amount and does not take into account any interest that has already been earned. For example, if you borrow $1,000 with a simple interest rate of 5%, you will owe $50 in interest after one year ($1,000 x 0.05 = $50).

Compound Interest

Compound interest, on the other hand, is a type of interest that is calculated based on the principal amount, interest rate, and time period, but also takes into account any interest that has already been earned. This means that the interest you earn on your initial investment or loan amount is added to the principal amount, and the interest is then calculated on the new, higher principal amount. For example, if you invest $1,000 with a compound interest rate of 5%, after one year, your investment will be worth $1,050 ($1,000 + $50 in interest earned).

Key Differences

The key difference between simple interest and compound interest is that compound interest takes into account the interest that has already been earned, while simple interest does not. This means that compound interest will typically result in higher earnings or higher costs compared to simple interest over time.

When to Use Simple Interest

Simple interest is typically used in financial instruments such as personal loans, auto loans, and short-term investments. Since simple interest does not take into account any interest that has already been earned, it is best suited for shorter-term financial transactions.

When to Use Compound Interest

Compound interest is typically used in financial instruments such as mortgages, long-term investments, and savings accounts. Since

Which is Better for You: Simple or Compound Interest?

Both have their advantages and disadvantages, and which one is better for you depends on your specific financial goals and circumstances.

Simple Interest

Simple interest is calculated on the principal amount of a loan or investment, and it remains the same throughout the entire term. This means that if you borrow $10,000 at an interest rate of 5% per year for five years, you will pay a total of $12,500 by the end of the term.

One advantage of simple interest is that it is straightforward and easy to understand. It also allows you to calculate the total amount of interest you will pay or receive upfront, making it easier to plan your finances.

However, simple interest is not as beneficial as compound interest in terms of long-term investments. This is because simple interest does not account for the interest earned on the interest itself. So, if you invested $10,000 at an interest rate of 5% per year for five years, you would earn a total of $2,500 in interest, resulting in a total of $12,500.

Compound Interest

Compound interest is calculated on the principal amount as well as the interest earned on it. This means that the interest earned is added to the principal amount, and interest is calculated on the new balance. This cycle continues throughout the entire term, resulting in a higher return on investment or a higher cost of borrowing.

One of the advantages of compound interest is that it can generate significant returns over time, especially for long-term investments. For example, if you invested $10,000 at an interest rate of 5% per year for 30 years, you would earn a total of $43,219 in interest, resulting in a total of $53,219. This is because the interest earned is reinvested, resulting in a higher return on investment.

However, compound interest can also work against you if you are borrowing money. This is because the interest is calculated on the principal amount as well as the interest accrued, resulting in a higher cost of borrowing over time.

Unlocking Better Interest Rates

Interest rates play a pivotal role in our financial lives, impacting everything from mortgages and loans to savings accounts and credit cards. Securing favorable interest rates can save you thousands of dollars over time and significantly impact your financial well-being. In this guide, we’ll explore actionable strategies to help you receive better interest rates on your loans and investments.

1. Strengthen Your Credit Score

Your credit score is a crucial factor in determining the interest rates you qualify for. Lenders use it to assess your creditworthiness. To improve your credit score:

- Pay bills on time.

- Reduce outstanding debts.

- Avoid opening too many new credit accounts.

- Review your credit report for errors and dispute inaccuracies.

A higher credit score often translates to lower interest rates on loans.

2. Comparison Shopping

Don’t settle for the first loan offer you receive. Instead, shop around and compare rates from multiple lenders. This applies to mortgages, personal loans, auto loans, and credit cards. Websites and apps can help you quickly compare rates and terms, allowing you to choose the most favorable option.

3. Increase Your Down Payment

When taking out a loan, a larger down payment can often secure a lower interest rate. For mortgages, a 20% down payment can help you avoid private mortgage insurance (PMI) and access better rates. Similarly, a larger down payment on a car loan can lead to reduced interest charges.

4. Build a Relationship with Your Bank

Establishing a long-term relationship with your bank or credit union can be advantageous. Loyalty may lead to preferential treatment, such as lower interest rates on loans and higher interest rates on savings accounts.

5. Refinance Existing Loans

If market conditions have changed since you took out a loan, consider refinancing. Refinancing a mortgage, for example, can lead to lower monthly payments and interest savings. Likewise, refinancing high-interest student loans with a lower-rate option can reduce your long-term costs.

6. Improve Debt-to-Income Ratio

Lenders often consider your debt-to-income (DTI) ratio when assessing loan applications. A lower DTI ratio (less debt relative to income) can make you a more attractive borrower. To improve your DTI ratio, focus on paying down existing debts and avoid taking on new ones.

7. Invest Wisely

When investing, seek out opportunities that offer competitive returns. Consider high-yield savings accounts, certificates of deposit (CDs), and investment vehicles that match your risk tolerance and financial goals. Maximizing your returns on investments can help grow your wealth faster.

8. Stay Informed

Monitor financial news and interest rate trends. Understanding market dynamics and central bank policies can help you make informed financial decisions. For example, you may decide to lock in a mortgage rate when rates are low.

9. Negotiate

Don’t be afraid to negotiate with lenders or financial institutions. Ask for better terms, and be prepared to leverage competing offers to your advantage. Lenders may be willing to match or beat a competitor’s rate to secure your business.

Simple Interest Loan Payment Calculator

When you’re seeking a straightforward way to calculate your loan payments, the Simple Interest Loan Payment Calculator is your trusted ally. This versatile tool empowers you to comprehend the true cost of borrowing by focusing on the fundamental concept of simple interest. In this article, we’ll explore how this calculator works and how it can help you make informed financial decisions.

The Role of the Simple Interest Loan Payment Calculator

This calculator is particularly valuable for those seeking loans with a simple interest structure, such as personal loans or car loans. Here’s how it works:

Enter Loan Details: Begin by inputting the principal amount, annual interest rate, and loan term (in years). This information forms the foundation for your calculations.

Calculate Interest: The calculator swiftly computes the total interest amount based on the provided details. It shows how much you’ll pay in interest over the life of the loan.

Estimate Monthly Payments: It breaks down your loan into monthly payments, helping you visualize the monthly financial commitment. You’ll see both the principal and interest components of each payment.

Explore Scenarios: Adjust the loan amount, interest rate, or term to see how changes impact your monthly payments and the total interest paid.

Benefits of Using the Simple Interest Loan Payment Calculator

Transparency: By focusing on simple interest, the calculator provides a clear breakdown of your payments, helping you understand the cost of borrowing.

Budget Planning: It helps you budget effectively by providing a detailed overview of your monthly obligations.

Comparison Tool: Easily compare different loan scenarios to choose the one that best aligns with your financial goals.

Simple Interest Only Loan Calculator

Some calculators offer a variation known as the Simple Interest Only Loan Calculator. This version allows you to calculate payments for loans where you pay only the interest during a specified period, typically the first few years. Afterward, you’ll start paying both principal and interest. It’s a useful tool when considering interest-only loans for specific financial strategies.

FAQ

What is simple interest?

Simple interest is a straightforward interest calculation method that is based on a fixed percentage rate applied to the principal amount. The interest rate remains constant throughout the term of the loan or investment, and the interest is calculated based only on the original principal.

How is simple interest calculated?

The simple interest calculation formula is simple: Interest = Principal x Interest rate x Time. This means that the amount of interest earned or paid is directly proportional to the principal, the interest rate, and the time period.

What is the difference between simple interest and compound interest?

The main difference between simple interest and compound interest is that compound interest is calculated based on the principal amount and the accumulated interest. This means that the interest earned is reinvested, resulting in a higher return on investment over time. On the other hand, simple interest does not take into account the interest earned on the principal, resulting in a lower overall return on investment.

What are the advantages of simple interest?

One of the main advantages of simple interest is that it is easy to calculate and understand. It also allows you to know exactly how much interest you will earn or pay upfront, making it easier to plan your finances. Simple interest is also a good option for short-term loans or investments.

What are the disadvantages of simple interest?

The main disadvantage of simple interest is that it does not take into account the interest earned on the interest itself. This means that you will earn a lower return on investment compared to compound interest over the long term. Simple interest is also not suitable for long-term loans or investments, as the returns are lower.

What are some examples of simple interest?

An example of simple interest is a $10,000 loan with a 5% interest rate over three years. The total interest paid over the three-year term would be $1,500, resulting in a total of $11,500.

Another example is a savings account with a $5,000 deposit and a 3% interest rate over one year. The total interest earned over the one-year period would be $150, resulting in a total of $5,150.

What factors affect simple interest rates?

Simple interest rates are affected by several factors, including inflation, market conditions, the lender’s risk assessment, and the borrower’s credit score. Generally, the better your credit score, the lower your interest rate will be.

Conclusion

In conclusion, having access to the right simple interest loan calculators can be instrumental in developing and optimizing your loan repayment strategy. The Simple Interest Loan Payment Calculator and Simple Interest Only Loan Calculator are invaluable tools that can help you evaluate your loan options, plan your repayment journey, and make informed decisions. By leveraging these calculators, you can simplify your loan repayment process and work towards a secure financial future.

Simple Interest Loan Payment Calculator – Simple Interest Only Loan Calculator

Legal Notices and Disclaimer

All Information contained in and produced by the ModernCalculators.com is provided for educational purposes only. This information should not be used for any Financial planning etc. Take the help from Financial experts for any Finace related Topics. This Website will not be responsible for any Financial loss etc.